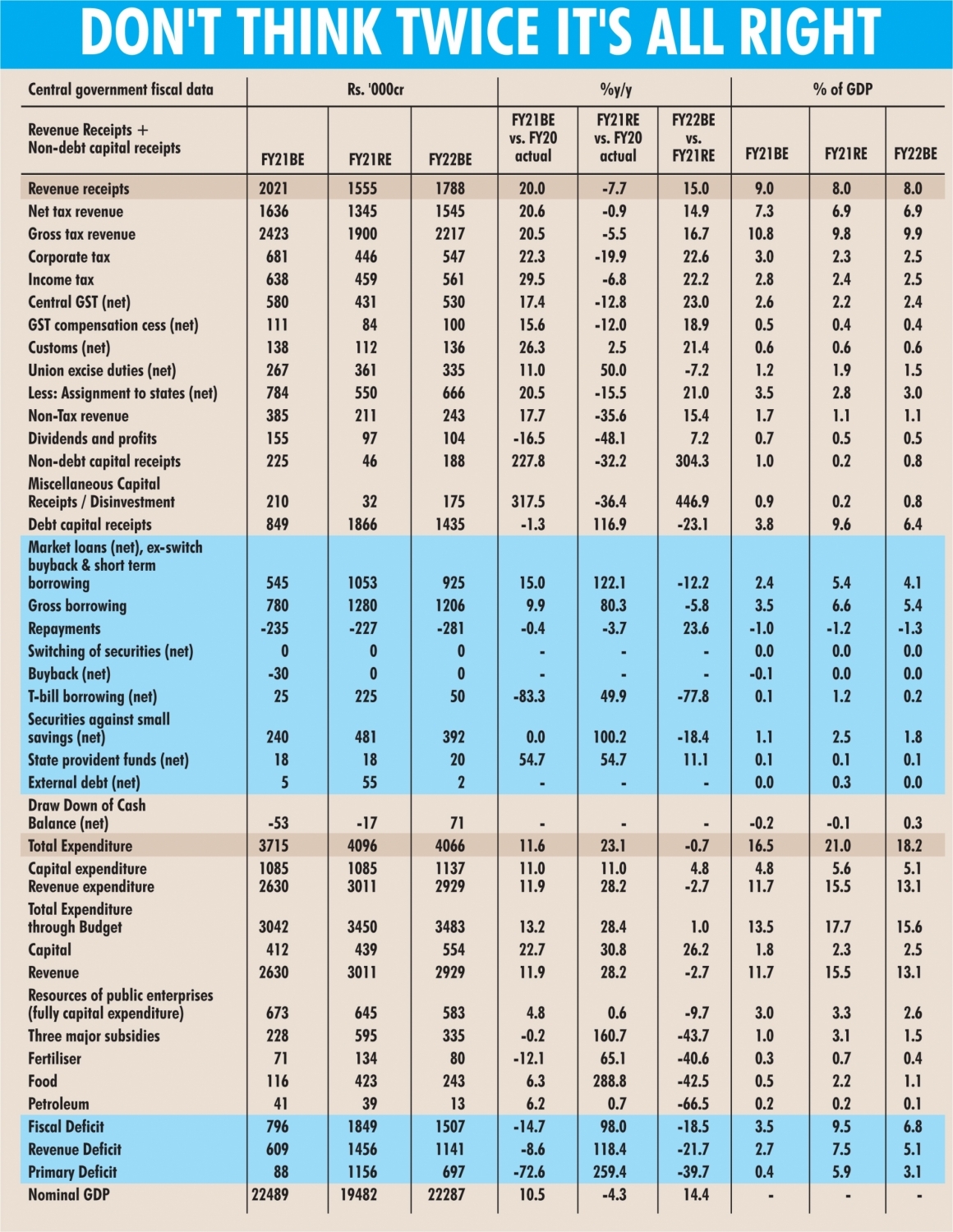

By Suyash Choudhary The budget exercise has tended to be seen with both wariness as well as weariness; the former because many a time the assumptions embedded dont pass muster with private forecasters and the latter because such an exercise is often accorded more importance than it usually deserves. However the present budget may just go down as a notable exception to these perceptions, especially the one about wariness. To that extent, it indeed signifies a break and is consistent with markets expectation of an exercise worthy of the unprecedented times that have been brought upon us. There are 2 points of context that need to be borne in mind when evaluating this budget: Basis a variety of factors including a multi-year growth slowdown and disappointments with respect to GST revenues, the degrees of freedom accorded to the finance minister in the past few budgets have been progressive diminishing. This has shown in many ways as, for instance, sometimes significant revisions from initial numbers, relying progressively more on other avenues of financing, and generally walking a more and more untenable tightrope of trade-offs. As is well documented India's direct fiscal response to the Covid crisis was somewhat modest when compared with many peers even in the emerging world. This was initially criticized but, given the sharp recovery seen recently, seems to have been the more prudent approach to follow. Also, the same sharp recovery has significantly bolstered government revenues now leading to a massive jump in government spending from the October � December quarter (of course growth and government spending are interlinked and mutually reinforcing). Given this context the ask from the budget broadly was to step up spending now that physical constraints to activity are rapidly diminishing in light of the apparent break in India between case load and mobility. This would entail an enhanced focus on welfare spending (health and health infrastructure included) to address the current situation as well as on high multiplier spending (capital expenditure) to sustain this upturn over future years. The means to do so were now more at hand given the relative fiscal conservatism of last year and with the recent upsurge in revenues. To us, the government has delivered on this and more; the added dimension being a potential realization that the current crisis as well as our better than anticipated fiscal situation gave a unique opportunity to clean up as well as to project conservatively. The advantages, which are plainly visible, are both a credible budget as well as ample degrees of freedom for the time ahead. The table shows the key data from the budget. The following items standout, and should be viewed in the context laid out above: Fiscal deficit for FY 21 at 9.5% and for FY 22 at 6.8% are both higher than market estimates (7% and 5.5% respectively). However, as can be seen from table a significant portion of an increase in spending comes from taking on the food subsidy bill on the budget instead of financing FCI (Food Corporation of India) via the NSSF (National Small Savings Fund). This in turn frees up NSSF resources which the government has used. Apart from this, capital spending through budget has been stepped up and is expected to go up further in the next financial year. Since most of the extra spending pertains to the subsidy clean up, expenditure growth through the budget falls back to a just 1% growth for FY 22 after having grown at 28.4% in FY 21. Even here, the quality dramatically improves as revenue expenditure falls back after the clean up to -2.7% while capital spending continues to grow robustly. Thus this budget exercise can hardly be called an expansionary one and therefore may have no negative implications at all for monetary policy (more on this below). Revenue forecasts are quite conservative and for the first time in a long time, market commentators may actually forecast a better realization than has been projected. Thus on a 14.4% growth in nominal GDP, gross tax revenue is projected to grow at 16.7%. Both these numbers may have some upside potential to them as the new year progresses. Similarly, given a heavy pipeline of large ticket items, disinvestment assumptions may not be too aggressive as well. Bond Market Takeaways Despite notable positives in the budget as discussed above, the bond market has understandably been disappointed for now. This is because of higher than expected fiscal deficit numbers leading to higher than expected gross borrowing numbers. The INR 80,000 crores extra borrowing for this year is especially a bolt from the blue for the bond market. This is because the government has been consistently running very high cash balances lately, revenues have picked up dramatically, and even though spending has gone up it hasn't been tracking anywhere close to what is required to yield the revised budget numbers. The difference of course is the one time clean up of the food subsidy financing that the government has chosen to undertake and as detailed above. Even for the next financial year, the bond market has been broadly working with a gross borrowing number between INR 10.5 � 11 lakh crores and the INR 12 lakh crores in the budget is certainly higher than expected. Finally, the future path to consolidation is also somewhat gradual with the government projecting a 5 year time frame to achieve below 4.5% deficit. That said, what needs to be kept in mind is that even a INR 11 lakh crore number (and states over and above this) was well outside the orderly absorptive capacity of local market participants and would have required active support from either RBI or FPIs or both. Looked at that way, the critical point here is to also examine whether the budget has potential to change RBI's view on support required. While we will know more at the next MPC (Monetary Policy Committee) shortly due, our own assessment is that for the reasons mentioned above the RBI is likely to view this budget as a positive outcome. Thus both the move towards greater transparency as well as the nature of incremental spending should provide more than adequate comfort to the central bank. The government can hardly be blamed for not being prudent especially as overall spending is hardly growing in FY 22 over FY 21's revised numbers. Thus our base case remains that RBI support will be forthcoming and the central bank will be wary of any disorderly unwind to the monetary transmission that has finally been working effectively over the past few quarters. It is also likely in our view that recent developments with respect to India's V shaped recovery alongside this budget and the general government approach of being consistent and sustainable with its fiscal response, will serve to better instead of worsen offshore perception of local Indian assets. In conclusion then, our views with respect to monetary policy remain that of a gradual normalization leading to a gentle bear flattening of the curve where the starting point is already a quite steep yield curve (for details refer https://idfcmf.com/article/3600). Bond yields have been almost continuously rising for the past few weeks since RBI's move to introduce variable reverse repo and today has seen another sharp uptick as well. From a valuation standpoint, our preferred segments (5 to 8 years, with overweight in 6 years within this) in our active duration strategies have become even more compulsive. A simple way to understand our thesis is to try to visualize what a 5 year government bond yield is likely to be 1 year from now. Given that approximately 6 year government bonds yield around 5.95% after today's move and applying the illustrative example detailed in the note referred to above, one can readily see that the bond market is already pricing in a lot. That said, an underlying requirement for realizing some sort of carry adjusted for duration risk is that bond yields in one's desired segments don't move around as aggressively as they have over the past month. It remains the view that with most of the repricing having been done, one may have scope for this requirement being met in the months ahead. (Suyash Choudhary is Head of Fixed Income, IDFC AMC. The views expressed are personal.)

Don't think twice, it's all right: Union Budget FY22

Don't think twice, it's all right: Union Budget FY22 . (IANS Infographics)